Manufacturing Cost Estimating: Tools, Strategies, and Best Practices

TL;DR: Manufacturing cost estimating has evolved with advanced software and real-time data, letting companies calculate total manufacturing costs, optimize manufacturing processes, and protect profits. This article explains key components, from direct materials to overhead costs, and explores tools, strategies, and real-world tips for improving accuracy, managing risk, and staying ahead in a fast-changing market.

What Is a Manufacturing Cost Estimate?

A manufacturing cost estimate is a forecast of all the expenses required to produce a finished product. It typically breaks down direct material costs, labor costs, and overhead costs. Generating an accurate manufacturing cost estimate is key to pricing products competitively, maintaining profitability, and ensuring business sustainability.

Accurate estimates help manufacturing businesses of all sizes avoid underpricing, reduce the risk of unprofitable orders, and improve production planning. With costs rising for raw materials, labor, and utilities, a detailed cost estimate forms the foundation for decision-making and competitive advantage.

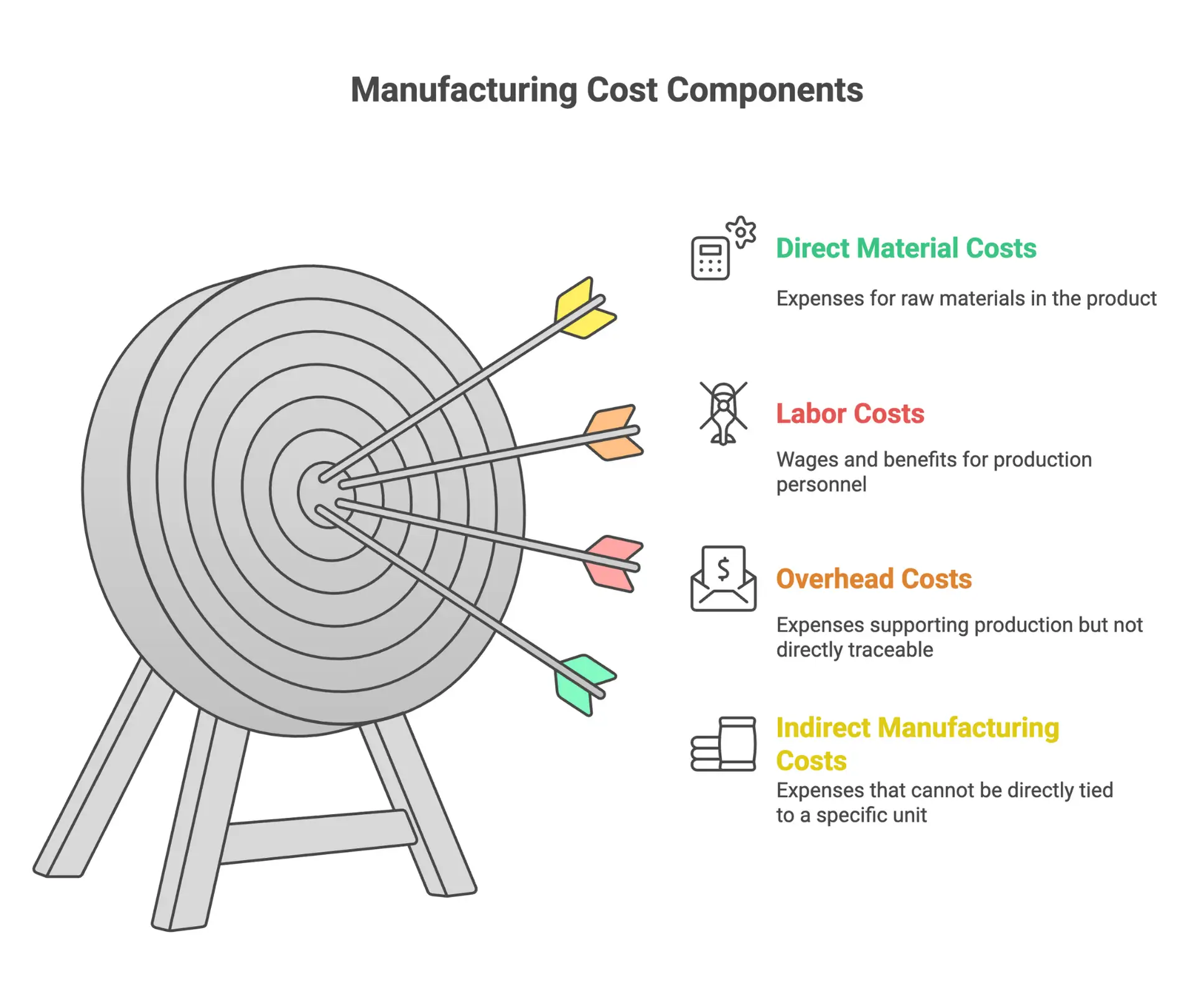

Components of Manufacturing Costs: Direct Materials, Labor, and Overhead

Understanding manufacturing costs starts with breaking them into core components:

Direct Material Costs

Direct material costs are the expenses for the raw materials that become part of the finished product. For example, if you manufacture furniture, the wood, fabric, and hardware are direct materials. Companies track direct material costs carefully, often with a detailed Bill of Materials (BOM) that lists every component required for production.

Direct materials are a significant part of the total manufacturing cost. The quality standards you set for materials impact not just expense but also waste. Higher quality materials usually cost more but may reduce waste or defects during production.

Labor Costs: Direct and Indirect

Labor costs cover the wages and benefits for all personnel involved in the production process. This includes:

- Direct labor: Workers who physically assemble or produce the product (machine operators, assemblers).

- Indirect labor: Support staff such as production supervisors, factory managers, quality control inspectors, and maintenance workers.

Indirect labor is often overlooked but can add up substantially. Training and turnover costs also factor into labor expenses, especially in industries with high staff turnover.

Overhead Costs & Manufacturing Overhead

Overhead costs are all expenses that support production but aren’t traced directly to a product. Manufacturing overhead covers items such as:

- Utility expenses like electricity and water for the manufacturing facility

- Depreciation and maintenance of equipment

- Factory rent or property taxes

- Indirect materials, such as lubricants and cleaning supplies used during the production process

- Shipping costs for incoming materials or finished products

Overhead costs can be divided further into fixed costs and variable costs:

- Fixed costs: Remain steady regardless of production volume (factory rent, salaried managers)

- Variable costs: Fluctuate with the level of production (raw material consumption, hourly labor)

Understanding the interplay between fixed and variable overhead expenses is crucial to calculating true production costs.

Indirect Manufacturing Costs

Indirect manufacturing costs are those expenses that cannot be directly tied to a specific unit but are necessary for running the manufacturing operation. These often include quality control, supervision, factory utilities, and insurance. Companies must regularly review indirect costs to keep overall manufacturing cost estimates accurate and prevent profit leaks.

How to Calculate Total Manufacturing Cost

To calculate total manufacturing cost, use this simple formula:

Total Manufacturing Cost = Direct Material Costs + Direct Labor Costs + Manufacturing Overhead

For example, if a company spends $150,000 on raw materials, $80,000 on direct labor, and $50,000 on manufacturing overhead in a month:

Total Manufacturing Cost = $150,000 + $80,000 + $50,000 = $280,000

Understanding your total manufacturing costs helps in setting realistic price points. It also supports the identification of inefficiencies and opportunities for cost-saving.

Detailed Example

Consider a business that produces 1,000 units of a finished product in a month. Suppose the following costs apply:

- Direct materials: $50,000

- Labor costs (direct + indirect): $30,000

- Manufacturing overhead: $20,000

Total manufacturing cost = $100,000

Cost per unit = $100,000 / 1,000 = $100

This per-unit calculation helps manufacturers set prices strategically and understand the impact of production volume on overall costs.

Manufacturing Costs vs. Production Costs: What’s the Difference?

Manufacturing costs include only the costs directly linked to creating products: direct materials, direct labor, and manufacturing overhead. Production costs, however, are broader. They cover every expense involved in the production process, from materials through labor, overhead, consumables, quality control, and logistics.

Production Costs: Key Elements

- Direct materials and consumables

- Direct and indirect labor

- Manufacturing overhead

- General overhead: administration, logistics, packaging, transportation, and shipping costs not always tied to manufacturing specifically

Variable vs. Fixed Costs

- Fixed overhead costs are stable across production volumes (factory rent, equipment depreciation).

- Variable costs (materials, energy, hourly labor hours) change with production volume.

Factoring in both fixed and variable costs, and separating them from indirect costs, is key for effective cost management.

How Quality Standards and Supplier Relationships Impact Manufacturing Costs

Quality standards affect material selection, quality control, and waste. Higher quality usually leads to greater expenses but may reduce the cost of rework or defect management.

Supplier factors, such as relationships, negotiation skills, and sourcing strategies, impact raw material and component prices significantly. Collaborating with suppliers from the design stage can create cost-saving opportunities.

A Bill of Materials (BOM) streamlines supplier negotiations by providing a detailed, itemized list of every component needed for the finished product.

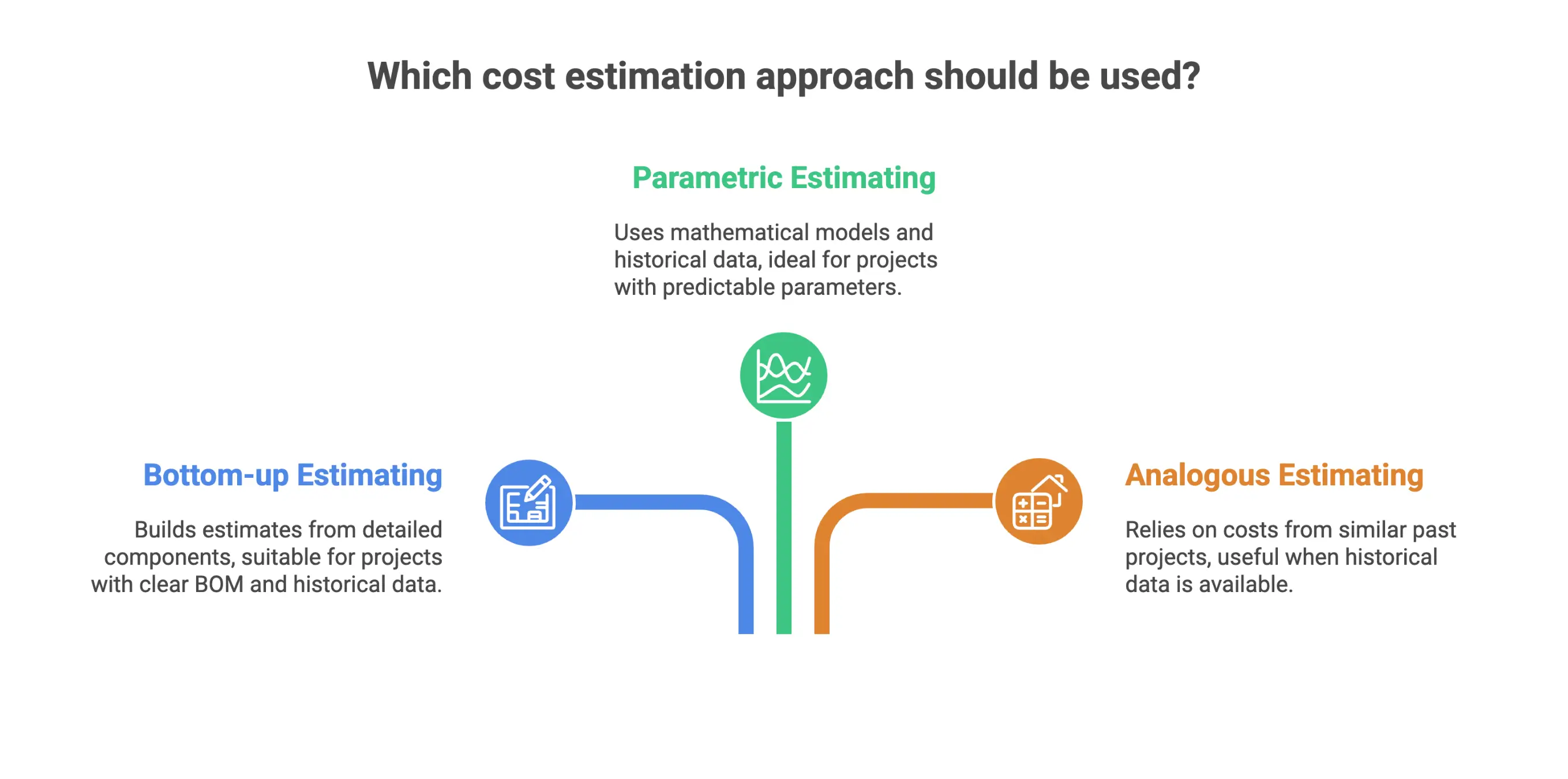

Manufacturing Cost Estimation Methodologies and Tools

Manufacturers use a range of methodologies and tools to generate accurate manufacturing cost estimates. Approaches can span from spreadsheet-based methods to database-driven platforms using historical data.

Common Approaches:

- Bottom-up estimating: Building estimates from the details of each product component or operation, often using a BOM and historical cost databases.

- Parametric estimating: Using mathematical models and historical data to predict costs based on production volume, material types, and process complexities.

- Analogous estimating: Relying on costs from similar past projects as a reference point.

Companies often combine these methods and refine them using simulation tools or integrated estimation software.

Specialized Cost Estimation Software

Dedicated cost estimation software for manufacturing businesses has been available since the 1980s. Modern solutions integrate engineering analytics, materials forecasting, and business cost management in one platform. Examples of such tools include CostOS and aPriori, offering everything from detailed raw materials analysis to real-time scenario planning.

Advanced Technology in Manufacturing Cost Estimating

Today’s manufacturing cost estimation leverages technologies like machine learning, simulation-driven cost estimation, and integration with design systems.

Machine Learning and Predictive Analytics

By analyzing vast sets of historical production data, machine learning models improve the ability to estimate direct costs, indirect costs, and total expenses for new and customized products. These systems reveal patterns and cost drivers not apparent through manual processes, allowing companies to forecast labor costs, raw material needs, and manufacturing overhead with greater confidence.

Advancements in artificial intelligence allow continuous improvement. As new data is collected from each production run, models learn and predictions become more precise.

Simulation-Driven Cost Estimation

Simulation-driven estimation tools let companies model new product designs, manufacturing processes, or production methods before committing resources. This approach supports:

- Exploring cost-optimized alternatives for product design

- Identifying opportunities for process improvement

- Testing scenarios for production volume shifts, labor costs, and raw materials usage

By integrating simulation with design to cost (DTC) strategies, teams can manage costs proactively from the earliest stages of product development.

Digital Twins and Real-Time Data Integration

A digital twin is a virtual model of your manufacturing facility that can simulate all steps of your production process. Real-time sensor data is fed into the model to reflect current equipment status, utility expenses, and material consumption. The result is improved visibility into manufacturing costs and bottlenecks, with the flexibility to adjust tactics on the fly.

Pairing digital twins with IoT technologies and BIM rendering engine tools delivers high-definition, interactive cost estimations, enhancing decision-making and efficiency.

Software Integration: Linking Cost Estimation with ERP Systems

Integrating cost estimation platforms with ERP systems enables seamless information flow between engineering, procurement, and finance. Advantages include:

- No manual entry or double-booking numbers

- Up-to-date cost data across the company

- Improved ability to calculate and manage total cost and total manufacturing cost

- Enhanced coordination for setting cost targets and tracking actual expenses

ERP integration for cost estimating brings these processes together, allowing instant responses to price changes, supplier shifts, or production adjustments.

Manufacturing Processes and Cost Optimization

Optimizing manufacturing processes is central to controlling manufacturing costs and improving profitability. Advanced cost estimation helps companies:

- Identify inefficiencies in the production process

- Manage direct and indirect manufacturing costs

- Keep product costs predictable across units manufactured

- Make better production method and design decisions

Lean manufacturing principles focus on eliminating waste throughout all production methods. Success in lean manufacturing is linked closely to effective cost estimation. By identifying and removing waste in materials, time, or unnecessary steps, manufacturers see both efficiency and cost benefits.

Practical Strategies:

- Use historical cost databases for benchmarking and improvement

- Collaborate with suppliers at the product design phase to uncover savings

- Adopt simulation-driven estimation tools to identify new efficiencies and cost reduction opportunities

- Monitor and optimize variable and fixed costs as production scales

Risk Management and Contingency Planning in Manufacturing Cost Estimates

Uncertainties, such as material price fluctuations, labor shortages, or equipment breakdowns, are inherent in manufacturing. Effective estimation means incorporating buffers and risk management strategies.

Common Practices:

- Add a contingency buffer of 5–10% of total estimated cost to absorb unforeseen expenses

- Regularly review estimates for changes in raw materials prices, utility expenses, or labor costs

- Use scenario analysis to determine the impact of supply chain disruptions

- Track and address waste and spoilage to keep finished product costs accurate

A robust risk management approach helps manufacturing businesses maintain margins, defend against unexpected setbacks, and determine when to adjust pricing.

Cost Estimation in Custom and Additive Manufacturing

Additive manufacturing and small-batch or custom production bring their own cost estimation challenges. Traditional formulas often miss hidden costs, such as special materials, intricate tooling, or variable labor needs.

Supporting Product Design and Design to Cost (DTC) Approaches

Modern cost estimation integrates deeply with product design. Using design to cost (DTC) methodologies lets product managers and designers set specific cost targets before production starts. Simulation-driven cost estimation during the design phase empowers teams to choose alternatives that meet budgets and quality standards.

When manufacturing cost estimation tools are fast, user-friendly, and actionable, they support real-time feedback throughout design and engineering changes. This agility helps deliver innovation without spiraling costs or missed targets.

Lean Manufacturing and the Drive Toward Optimal Production Costs

Lean manufacturing emerged as a major cost optimization strategy, rooted in improving the efficiency of Japanese manufacturers. It focuses on eliminating waste in unused materials, labor inefficiencies, or steps that do not add value to the final product.

Lean’s success depends on recognizing inefficiencies, identifying waste, and creating looped feedback between cost estimates and actual outcomes. Advanced technologies and cost estimation software provide the transparency and actionable insights necessary for ongoing improvement, helping teams manage total manufacturing and production costs proactively.

Frequently Asked Questions

What is included in manufacturing costs?

Manufacturing costs include direct materials, direct and indirect labor, and manufacturing overhead. Overhead costs comprise expenses necessary for production that aren’t directly tied to a single unit, such as utilities, equipment depreciation, and indirect support staff.

How do you calculate the total manufacturing cost?

Add up all your direct material costs, both direct and indirect labor costs, and manufacturing overhead for a given period. This sum gives you the total manufacturing cost, essential for setting prices and understanding your production profitability.

What’s the difference between manufacturing costs and production costs?

Manufacturing costs focus only on expenses directly related to turning raw materials into finished product (materials, labor, overhead). Production costs are broader, covering everything involved in producing and delivering a product, such as logistics, shipping, and quality testing.

Why are indirect costs important in manufacturing cost estimation?

Indirect costs, such as quality control, supervision, and facility utilities, are necessary for production but cannot be traced easily to specific products. Failing to account for indirect manufacturing costs can lead to underpricing and loss of profitability.

How can manufacturers identify cost-saving opportunities?

Analyze waste and inefficiencies in the production process, benchmark against historical cost data, and use simulation tools to test new production methods or materials. Collaborating with suppliers during the design phase and reviewing BOMs are also effective ways to optimize costs.

What is the role of labor costs in manufacturing?

Labor costs, including both direct (operators, assemblers) and indirect (supervisors, QA, maintenance), are a major part of the total manufacturing cost. Monitoring training and turnover expenses helps improve labor efficiency.

How does software improve manufacturing cost estimation?

Modern cost estimation software is quick, integrates with ERP systems for real-time updates, offers actionable insights, and supports simulation-driven design. This makes it easier to calculate costs, run scenarios, and manage profitability in dynamic manufacturing environments.

How does lean manufacturing relate to manufacturing cost estimates?

Lean manufacturing stresses waste elimination and process efficiency. Effective cost estimation methods are critical for identifying areas where resources, time, or costs can be reduced, making lean initiatives more successful and sustainable.

Do manufacturing cost estimates need a contingency buffer?

Yes. Adding a 5–10% buffer for unforeseen costs, such as price hikes or supply chain delays, is common practice. This helps prevent surprises from eroding margins and supports better contingency planning.

What factors influence the cost of raw materials?

Supplier relationships, negotiation skills, global commodity prices, and sourcing strategies all impact raw material prices. Maintaining strong supplier partnerships and tracking market trends help control this major cost driver.

How do companies manage quality standards without overspending?

By setting clear quality targets and integrating cost estimation into the product design process, companies can balance high standards with affordable material and production choices. Simulation-driven tools support informed decision-making without unnecessary expense.

What is a Bill of Materials (BOM) and why does it matter?

A BOM is a detailed, itemized list of every required component, material, and subassembly for manufacturing a product. It’s the foundation for accurate cost estimates, effective supplier negotiations, and streamlined production.

Conclusion

Modern manufacturing cost estimation blends old expertise with new technology, empowering companies to calculate total manufacturing cost, optimize manufacturing processes, and improve margins. By understanding all cost drivers, including direct materials, labor, overhead, and indirect costs, manufacturers can identify opportunities for efficiency and build a resilient, competitive business.

Ready to optimize your estimates? Explore Nomitech’s full suite, or get in touch to discover solutions that fit your company’s needs.

Stay Up to Date

Subscribe to our Newsletter today and receive the latest updates, trends, expert insights, and exclusive offers tailored to your specific industry.