Cost Estimating vs. Project Accounting: Key Differences & Integration

TL;DR: Cost estimating predicts what a project is likely to cost before the work kicks off, while project accounting tracks what’s actually being spent as things progress. Bridging these two worlds is key to keeping project costs on track, managing risk, and creating a culture of continuous improvement for project managers.

Introduction: Understanding Cost Estimating vs. Project Accounting

Keeping large project costs on budget shouldn’t feel like you’re herding cats, but for many project managers it does. Too often, initial cost estimates sit in one system while real expenses live in another, leaving those steering project finances blind to where things are drifting off course. Add in tighter deadlines, stretched resources, indirect and direct costs, and scattered financial reports, and it’s easy to see how cost overruns and unexpected project expenses sneak in.

Today, there’s almost no wiggle room for error in project management. That’s why closing the gap between early cost estimation and the nitty-gritty of daily project accounting isn’t just a “nice to have.” It’s the difference between profit and pain. When project managers see both sides clearly, they can catch projected versus actual costs before they snowball, enabling better cost control, resource allocation, and smarter decisions as the project progresses.

In this article, we’ll untangle what cost estimating and project accounting each bring to the table, and more importantly, show how tools like CostOS let you connect those dots. With live cost tracking wired into your estimates, leaders can spot trouble early, sharpen their project budgets, and build a cycle of learning that pays off on every particular project.

If you want results you can count on, not just tidy spreadsheets, let’s dig into how integrated project cost accounting and cost management put you back in control.

What is Cost Estimating in Project Management?

Cost estimation in project management is the process of predicting the financial investment required to complete a project successfully. Accurate cost estimation serves as the cornerstone of effective project management. It allows project managers to determine the financial requirements of a project and allocate resources efficiently. Comprehensive cost estimate practices help minimize resource shortages or surpluses and create project budgets covering all project aspects. Accurate cost estimates also help project managers navigate resource allocation, scope changes, and cost control decisions, reducing risk and preventing unexpected budget overruns as the project progresses.

Project managers must make critical decisions throughout the project lifecycle, relying on the accuracy of cost estimates to guide project finances. Cost estimation is not just about a starting number; it is pivotal for managing direct and indirect costs, tracking progress, and ensuring the project’s financial health.

Defining Cost Estimating and Project Accounting

Imagine cost estimating and project accounting as the bookends of a project’s financial story. One sets the target, the other tracks the journey. Let’s break down the essential differences and how they interact for successful cost control and project planning.

What Is a Cost Estimate?

A cost estimate comes first, before a single hour is logged or a shipment is ordered. At this point in the estimation process, the focus is on predicting what the project will cost, relying on hard-won experience, project scope, past projects, and the job’s requirements. The goal? Build a project budget that’s as close to reality as possible, giving everyone—from onsite leads to project managers and stakeholders—confidence to move forward.

As Bhadani's Recorded Lectures explains, cost estimation is part science, part seasoned guesswork, often backed up these days by cost estimating software for added speed and accuracy. It involves direct costs (like materials and labor costs), indirect costs (such as overhead costs), and the scope of work.

What Is Project Accounting?

Project accounting picks up where cost estimating leaves off. Once work begins, project accountants or controllers keep tabs on actual costs, labor costs, materials, equipment, subcontracts, right down to the last invoice. Unlike general financial accounting, which blurs everything together, project cost accounting focuses on each project by project basis. It gives project managers the ability to track the costs incurred as the project progresses and provides financial transparency through detailed financial reports. The project accounting process includes tracking revenue recognition, costs, and resource allocation for every deliverable.

Why Both Matter: The Value for Project Managers

Here’s the thing: mature organizations do not choose between cost estimation and project cost accounting, they use both to their advantage.

- Cost estimating sets the project scope, plans the project budget, and prepares the team for resource allocation and risk.

- Project accounting delivers real-time financial reports, controls costs, and flags budget overruns or variances as they develop.

A feedback loop between accurate cost estimation and project accounting enables cost control, successful project management, and smarter decisions on future projects. This synergy allows teams to compare estimated costs to actual costs, dig into the reasons behind variances, and refine the project accounting process flow for continuous improvement. Linking both creates a self-improving framework for project control, minimizing cost overruns and driving project success.

The Process of Cost Estimating: Laying the Financial Foundation

Strong project financial management begins, and sometimes succeeds or fails, with cost estimation. Here’s how top project managers approach the challenge of building accurate cost estimates and comprehensive project cost estimates.

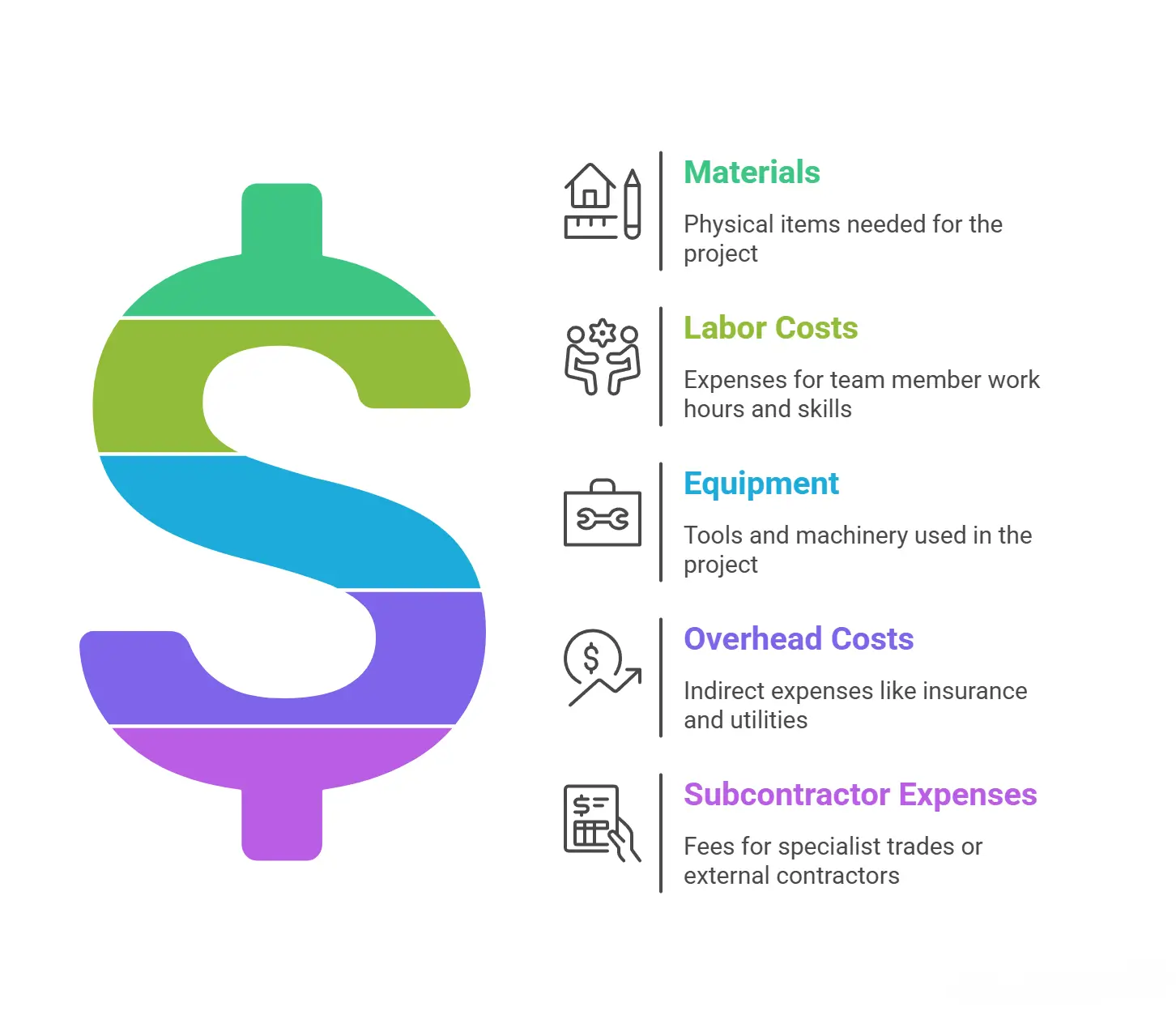

Key Elements of a Comprehensive Cost Estimate

A reliable cost estimate means covering every angle, especially the direct and indirect costs that make up the total project cost.

- Materials: All physical items required for the project scope.

- Labor costs: The work hours, skills, and pay rates for every team member.

- Equipment: Gear in use, whether rented, owned, or transferred from similar past projects.

- Overhead costs: Indirect costs like insurance, utilities, and site management.

- Subcontractor expenses: Fees for specialist trades or external contractors.

Miss any link, and you risk faulty project costs. Smart project managers weave these elements together for accurate cost estimation that holds up in execution. Many rely on a centralized cost estimating database updated with each construction project.

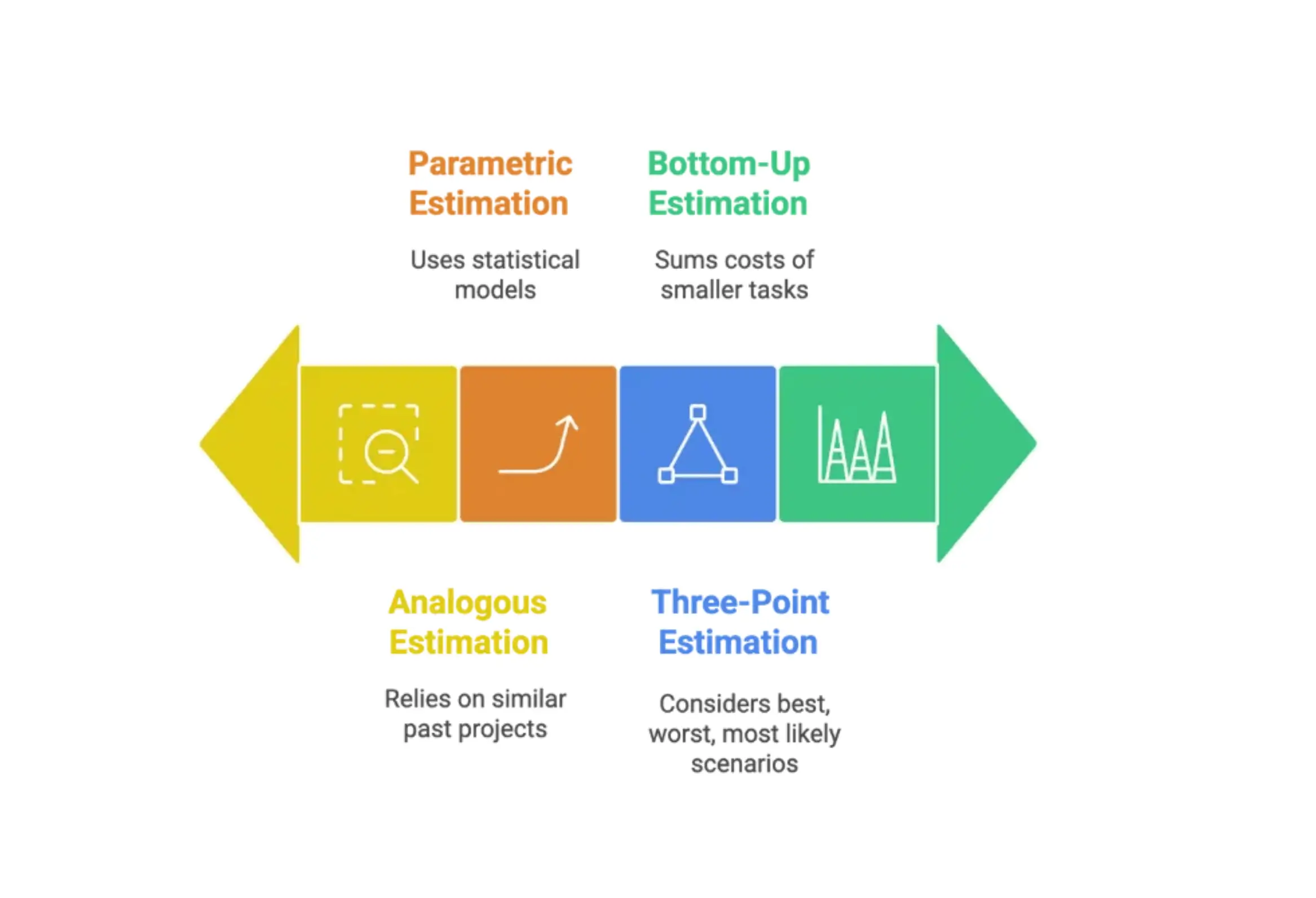

Cost Estimation Techniques

Multiple cost estimation approaches exist for project managers:

- Analogous estimation: Uses historical data from similar past projects to forecast costs.

- Bottom-up estimation: Breaks the project into smaller tasks or work packages, estimating costs for each, and summing for the total project cost.

- Parametric estimation: Uses mathematical models or statistical techniques to estimate costs based on specific project parameters. See parametric estimating method.

- Three-point estimation: Accounts for uncertainty by considering best-case, worst-case, and most-likely scenarios.

Combining these techniques and documenting assumptions ensures all stakeholders are aligned and increases accuracy. Reliable data, especially historical data, is crucial for cost estimation, while contingency reserves help account for unforeseen risks or anticipated future costs.

Why Accurate Cost Estimation Is Crucial for Project Success

If a project runs out of resources, it will likely fail. Putting in the effort upfront with comprehensive cost estimates helps project managers allocate resources efficiently and protect project finances. Continuous monitoring, using project management software with real-time tracking, and refining cost estimates throughout the project lifecycle are essential for staying on budget.

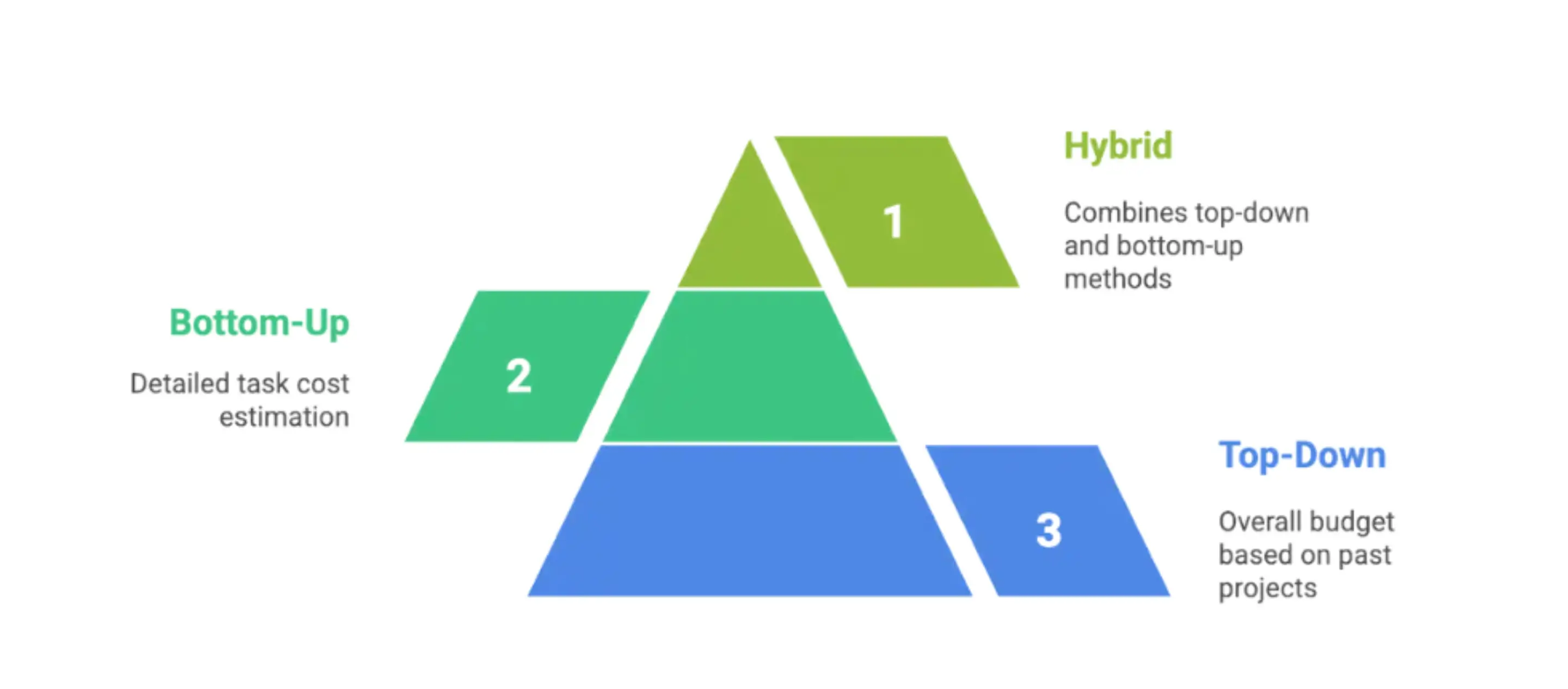

Estimation Methodologies: Top-Down vs. Bottom-Up

Project managers generally use top-down or bottom-up approaches for cost estimation, depending on the project phase:

- Top-down estimation: Starts with an overall project budget, often based on similar past projects or benchmarks. Useful in the early stages, when project scope and project costs are less defined.

- Bottom-up estimation: Builds from the ground up, estimating every task’s cost for a more detailed projected total project cost. Time-consuming but precise and useful for well-defined scopes.

- Hybrid approaches: Many teams combine both. They create a rough cost estimate using top-down methods, then switch to bottom-up as plans become clearer.

Leveraging Historical Data and Technology in Cost Estimation

Digital tools and historical project data have transformed cost estimation accuracy. Anchoring your estimates to actual costs from completed projects avoids wishful thinking. Advanced AI-powered estimating software can leverage XGBoost algorithms and past projects to predict cost drivers and risks.

By combining expertise, technology, and reliable historical data, project managers create accurate cost estimates even when designs are incomplete, driving cost savings, minimizing budget overruns, and sharpening resource allocation throughout the project lifecycle.

Project Accounting: Tracking and Managing Financial Performance

If cost estimation sets the course, project accounting is your GPS for the journey. Detailed tracking of project costs is critical for every step, from budget creation to completion, especially for construction companies and multi-phase project management.

The Project Accounting Process Flow

The project accounting process begins with an initial budget estimation. As the project progresses, accountants systematically track all costs incurred, including direct costs, indirect costs, revenue recognition, and financial transactions. This ongoing process creates detailed financial reports that inform project managers about their project's financial health.

Key steps in project accounting include:

- Comparing current project costs to the project budget and estimated costs.

- Flagging cost overruns, early signs of trouble, or variances in spend.

- Moving resources or adjusting scope to maintain strong cost control.

- Generating detailed billing, tracking time, labor costs, and materials.

- Assigning costs to every deliverable in the project accounting system.

When managed properly, project accounting tracks costs and revenue for each particular project, helping managers make informed decisions quickly.

Why Project Cost Accounting Is Essential for Project Managers

Project accounting is a strategic method of financial reporting and control designed for projects. It gives project managers a transparent, real-time view of project finances and financial performance. Project accounting focuses on the granular details:

- Each project is treated as an independent profit center, revealing stars and underperformers.

- Detailed tracking of project costs and performance enables effective project control and supports successful project management.

- Project accounting helps businesses manage costs, monitor profitability, generate financial reports, and improve decision-making.

Utilizing dedicated project accounting software enables project managers to track project expenses, manage project budgets, and benchmark across similar past projects, delivering data for continual project planning improvements.

Project-Specific Financial Insight vs. Organization-Wide Accounting

General financial accounting aggregates everything for company-wide records. In contrast, project accounting zooms in on a project by project basis, enabling:

- Analysis of costs incurred, revenue, and profit for every project or client.

- Spotting trends and making informed decisions about resource allocation.

- Enabling accurate forecasts and quick response to budget overruns or performance gaps.

This targeted visibility is what empowers project managers to track progress, keep costs under control, and drive projects toward their goals.

Construction Cost Accounting and Job Costing

No field uses project accounting like the construction industry. Job costing breaks down every construction project into labor, equipment, material, and subcontractor line items, giving teams granular control over construction costs.

NetSuite highlights construction’s unique approach:

- Establishing separate accounting systems for every construction project.

- Matching costs and revenue at the project level for clear profit snapshots.

- Tracking job-specific overhead costs, labor costs, and direct costs.

- Using dashboards and project accounting software for real-time updates.

For construction companies, job costing doesn’t just inform profitability. It enables proactive troubleshooting, resource allocation, and cost savings through early warning and better control.

Cost Planning: Bridging the Gap Between Estimates and Actuals

If cost estimation sets the starting line and project accounting captures the finish, then cost planning is what gets project managers from start to finish without losing track of project goals or financial health.

Cost planning bridges the estimate with actual costs throughout the project lifecycle. Effective cost planning keeps project budgets alive and adaptable as circumstances shift during execution.

Continuous Budget Refinement and Cost Control

Project budgets that are never reviewed are quickly outdated. Effective project control and planning require:

- Running frequent check-ins comparing actual costs to project cost estimates.

- Adjusting resource allocation and funding as realities shift.

- Updating project budget projections and reflecting continuous learning in future projects.

Contruent notes that cost planning must be ongoing, not a one-time calculation. With project management and accounting platforms that combine real-time spend and project budgets, project managers can spot issues, respond early, and keep projects on target.

Technological Solutions: Enhancing Accuracy and Efficiency

Technology is critical for modern project cost management. Accurate, up-to-date project costs depend on systems that unify cost estimating, project cost accounting, and real-time scenario modeling for every project.

Integrating Real-Time Data and Scenario Simulation for Project Control

Today’s project estimating software combines all cost drivers, such as labor costs, materials, and overhead costs, into one intelligent system for project managers. Powerful simulation tools allow for scenario planning, such as testing material substitutions or scheduling changes, before decisions are made.

Project managers can now:

- Pressure-test plans and scenarios before spending.

- Adjust budgets and allocations on-the-fly.

- Compare estimated costs against actual costs at every milestone.

- Control project costs proactively, improving overall project performance.

When your system feeds actual project accounting data directly into cost estimating databases, every completed contract or construction project refines and improves the next cost estimate. Software such as CostOS cost estimating is designed for this integration, taking project cost estimation and accounting to new levels of accuracy and agility.

Cost Estimating vs. Project Accounting: A Comparative Framework

Cost estimating and project accounting are both critical for effective project management, but their true value comes when combined in integrated project cost control.

Key Differences Between Cost Estimating and Project Accounting

- Timing: Cost estimation happens in the early stages, forming the foundation for financial planning. Project accounting operates throughout project execution, continuously tracking costs incurred.

- Purpose: Cost estimating predicts the total project cost and prepares the budget. Project accounting tracks every financial transaction and cost as the project progresses.

- Reporting: Project accounting uses specialized processes not typically found in standard financial accounting, delivering project-by-project granularity.

- Focus: Cost estimation sets expectations; project accounting monitors actual costs, controlling financial risk.

Both play essential roles in project management. Accurate cost estimates help avoid unexpected costs. Project accounting ensures project costs are watched, controlled, and optimized as projects move forward.

Practical Intersections for Project Managers

The value of integrating cost estimation and accounting is that project managers and teams can:

- Use project cost estimates and actual costs to build better budgets.

- Compare estimated costs and project budgets to ongoing results for early risk identification.

- Feed variance data back into cost estimation processes to improve accuracy for future projects.

A strong feedback loop between estimate and performance supports continuous improvement, greater resource efficiency, and more reliable delivery times.

Optimizing Project Delivery through Integrated Insights

Merging cost estimating and project accounting builds a feedback system for tightening project budgets over time. As Contruent describes, bringing accounting data into estimation tools gives project managers access to up-to-the-minute, realistic baselines.

Project teams benefit through:

- More accurate project cost estimates informed by historical data and actual performance.

- Immediate insight into project progress and variances for responsive risk control.

- Faster decisions and adjustments for budget overruns as they emerge.

- Consistent refinement of cost estimation and project planning processes with each completed project.

This predict-measure-adjust approach turns project finances into a strategic advantage, supporting successful project management and cost savings for the organization.

Industry Applications: Project Cost Control in Construction and Beyond

Approaches to cost estimating and project accounting may vary by industry, but the core principles benefit all project-driven environments.

Construction Cost Estimation: The Gold Standard for Project Financial Control

The construction industry is the archetype for rigorous project control, tying project cost estimation and accounting into a single workflow. Job costing, as highlighted by NetSuite, allows teams to:

- Compare project budget to live spending at every stage.

- Address cost overruns and unexpected changes in real-time.

- Track individual projects and phases to maintain project goals and financial health.

- Adapt to material, schedule, or scope changes with minimal disruption.

Modern construction cost estimation tools make it practical for managers to implement similar best practices across the industry.

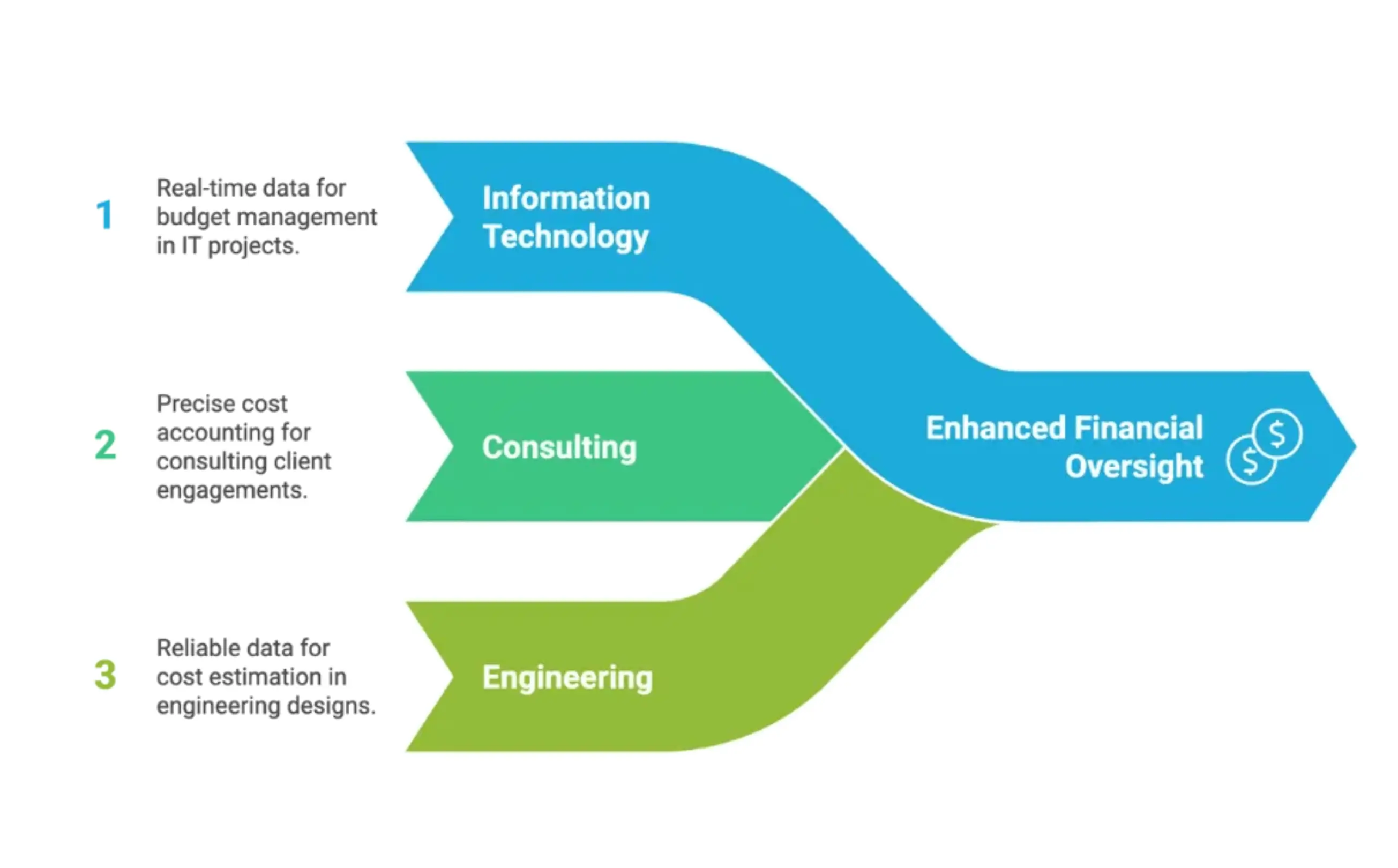

Expanding Lessons to Other Project-Driven Industries

While construction offers the most developed model, fields like IT, consulting, engineering, and more are adopting these project cost control methods. As RCS Construction Management illustrates, building clear cost boundaries, tracking project finances, and learning from each project applies in any environment where budget overruns can derail progress.

Example advantages include:

- Information Technology: Using historical data and real-time tracking for budgets on rapidly evolving requirements.

- Consulting: Project cost accounting for every client engagement, allowing precise financial oversight.

- Engineering: Incorporating reliable data and cost estimation techniques for complex designs.

Industry-focused project cost estimation platforms, like Nomitech’s solutions, are adaptable to any sector where project managers demand accurate estimates, strong cost control, and reliable project delivery.

Mastering Cost Estimation in Project Management

Effective cost estimation is more than just crunching numbers. It requires a deep understanding of project scope, the use of reliable historical data and expert input, and the right mix of estimation techniques. Here’s what to keep top of mind for project managers striving for accurate project estimate results and successful project management:

- Collaborate with experts to gather insight and validate assumptions.

- Use analogous, bottom-up, parametric, and three-point estimation methods together.

- Incorporate contingency reserves for risk, uncertainty, and unexpected costs.

- Document all assumptions and update them as the project progresses.

Combining these elements creates a foundation for project managers to allocate resources better, minimize the risk of resource shortages, and craft comprehensive and realistic project budgets.

Project Accounting Fundamentals for Successful Project Management

Project accounting is more than cost tracking. It is about achieving transparency and effective project control. Key practices for project managers include:

- Establishing dedicated project cost accounting systems for each project.

- Tracking all costs incurred, including labor costs, overhead costs, and materials.

- Comparing actual costs and projected totals to spot deviations early.

- Utilizing project accounting software to automate revenue recognition and financial reporting.

Strong project accounting structures set the stage for successful project management by sharpening financial analysis and supporting smart decisions as projects unfold.

How Accurate Cost Estimation and Project Cost Accounting Improve Outcomes

Bridging the gap between estimation and accounting is critical for any project manager responsible for achieving their project’s financial goals. By integrating cost estimation with project cost accounting:

- Project managers and stakeholders gain clear, real-time financial visibility.

- Continuous improvement is supported by learning from each project’s variance data.

- Critical decisions across the project lifecycle, including scope, resource allocation, and priorities, are informed by reliable financial data.

- Risk management and cost control become proactive rather than reactive.

This integrated approach strengthens every phase of the project lifecycle, resulting in more consistent outcomes.

The Project Accounting Process Flow: From Budgeting to Reporting

The project accounting process is cyclical, not linear:

- Initial Project Budgeting: Using accurate estimation methods and historical data to set expectations for the total project cost.

- Real-Time Tracking: Monitoring and controlling costs as the project progresses, recording every transaction and cost incurred.

- Variance Analysis: Comparing actual costs to budget, identifying cost overruns, and determining underlying causes.

- Reporting and Feedback: Providing detailed financial reports to project managers and informing accurate estimates for future projects.

- Continuous Improvement: Applying learnings to the next project to increase estimation accuracy and improve cost control.

This closed-loop process lies at the heart of successful project management in every sector.

Frequently Asked Questions

What is the main difference between cost estimating and project accounting?

Cost estimating predicts the total project cost and project budget required before work begins, often using data from past projects and project scope analysis. Project accounting manages what’s actually being spent as the project progresses, providing financial clarity throughout the project lifecycle.

How does connecting cost estimating with project accounting benefit project managers?

Linking forecasts to actuals allows project managers to see budget gaps early, make corrections before overruns occur, and refine cost estimates based on real project costs and performance.

Why is cost planning important in the lifecycle of a project?

Cost planning connects your earliest cost estimates with the live financial data coming in. It’s a continuous process of updating, adjusting, and steering the project budget toward a successful outcome.

How do technology solutions improve cost estimating and project cost accounting?

Modern project management software integrates real-time data, scenario simulation, and historical benchmarks. This streamlines cost estimation, enables seamless tracking of spend and actual costs, and allows for sharper cost control on every project.

Are these processes only relevant for construction projects?

Not at all. While construction set the standard for project financial control, project accounting and cost estimation support every project-driven industry—IT, engineering, consulting, and others—all benefit from accurate project estimate practices and reliable financial oversight.

Conclusion: Achieving Project Success through Informed Financial Management

Projects succeed not by chance, but by building on solid financial foundations. Uniting cost estimation, project cost accounting, and cost control is essential for project managers seeking predictable, profitable results. When accurate cost estimates inform detailed project accounting, organizations unlock a self-improving cycle. This delivers accurate budgets, timely reporting, and responsive adjustments for every project.

Best Practices for Bridging the Cost Estimating vs. Project Accounting Gap

Looking to tighten your project cost control and strengthen project performance? Here’s a proven list for project managers:

- Integrate software tools that connect cost estimation, project cost accounting, and reporting for higher accuracy and fewer surprises. BuildOps and CostOS cost estimating are strong options.

- Encourage ongoing communication between estimators, accountants, and project managers to spot red flags early and enable faster fixes.

- Standardize your data structures so everyone speaks the same language, supporting the seamless movement of financial data from estimates to invoicing.

- Establish tight feedback loops: feed on-the-ground costs back to project estimators, supporting accurate project estimates for future jobs.

- Cross-train teams across estimation and accounting skills, building shared understanding and supporting less siloed project management.

These steps help project managers achieve consistent project goals, minimizing cost overruns and supporting successful delivery.

Ready to Take the Next Step?

If you’re exploring new cost estimation and project accounting platforms, take a look at Nomitech’s solutions or reach out to see how the right fit can streamline your workflows and help project managers master cost control.

Cost estimation and project accounting are mutually reinforcing pillars of successful project management. By mastering both, project managers and organizations position themselves for consistent wins and robust financial control on every project.

Stay Up to Date

Subscribe to our Newsletter today and receive the latest updates, trends, expert insights, and exclusive offers tailored to your specific industry.